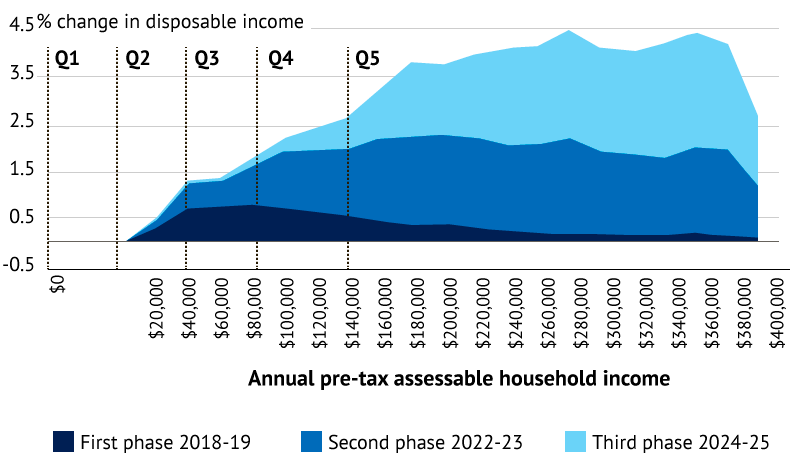

Which workers will benefit most from $140 billion income tax plan

Voters in Labor-held seats will be some of the biggest beneficiaries of the Turnbull government’s income tax overhaul, according to new data which also reveals which workers will benefit most from the $140 billion plan. Analysis shows residents of the federal electorate of Sydney, held… Read More »Which workers will benefit most from $140 billion income tax plan